7 Best Out-of-State 529 Plans for Wyoming Students (No In-State 529 Option)

Wyoming doesn’t sponsor its own 529 college-savings plan, and the state charges zero income tax. That double freedom lets you shop any plan nationwide without giving up a home-state deduction. Choice, however, can feel paralyzing—fees, past performance, and new SECURE 2.0 rollover rules stack up fast. We compared every major direct-sold option so you can pick a Wyoming-friendly 529 with confidence.

In the pages ahead, we will:

- Explain, in plain English, the criteria that separate a great plan from a merely good one.

- Rank the seven standouts that rose to the top in 2026.

- Show you, step by step, how to decide which plan fits your family’s goals and comfort level.

Short, punchy paragraphs keep the journey easy on the eyes. Light comparisons and a quick-scan table give you the data without the headache.

Ready to turn tax-free freedom into focused action? Let’s dive in.

How we picked the winners

Wyoming savers care about two things above all: cost and consistent returns. With no state tax break at stake, we built a five-factor scorecard that reflects that reality.

1. Fees (35 percent weight)

Every basis point saved stays in your pocket. We reviewed the latest disclosure booklets and flagged any age-based or 100 percent equity option that costs more than 0.40 percent. Understanding personal finance planning helps families evaluate 529 fee structures and make smarter long-term decisions about college savings and investment returns. Plans such as Illinois Bright Start at 0.06 percent and New York Direct at 0.11 percent set the benchmark for an automatic A plus.

2. Performance (25 percent weight)

Morningstar’s 2025 analyst review named only five Gold-medal 529s nationwide. We cross-checked each finalist’s five- and ten-year record against peers to confirm that low fees translated into real-world gains.

3. Investment menu (15 percent weight)

Choice matters only when it is quality. We rewarded plans that pair broad index tracks with a few thoughtful extras—such as Utah’s custom mix builder or Ohio’s bank-rate stable-value fund—and docked those that bury savers in pricey niche funds.

4. Ease of use (15 percent weight)

Good intentions die on clunky websites. We opened test accounts, timed enrollment, checked mobile access, and verified that each plan enables automatic deposits and a shareable gifting link.

5. Extras and flexibility (10 percent weight)

Small perks broke close ties: ESG tracks, newborn bonuses, high contribution ceilings, and clear guidance on the new 529-to-Roth rollover rule that started in 2024.

Scores from all five buckets rolled into a clean 100-point scale. The result is a ranking you can trust, grounded in hard numbers, not marketing hype.

1. Illinois Bright Start 529: our top pick

Bright Start succeeds by nailing the basics.

Its cheapest index portfolio costs just 0.06 percent a year, lower than the Vanguard-run Nevada plan and well below the national average. On ten thousand dollars invested for 18 years, total fees would be about sixty dollars.

Low cost matters only if returns follow. Morningstar’s 2025 report awarded Bright Start a Gold rating for “compelling investment options that are also highly cost-effective.” The age-based tracks land in the top quartile over five and ten years, showing that price discipline translates into real gains.

Choice is broad yet focused. Three age-based glidepaths cover aggressive, moderate, and conservative settings. Savers who want more control can build a custom mix from Vanguard, BlackRock, and DFA funds.

Opening an account is quick: no minimum balance, a fifteen-minute online form, and a shareable gifting link for relatives.

For Illinois parents, the Illinois First Steps Program sweetens the deal by adding a one-time $50 seed deposit to Bright Start accounts opened for children born or adopted in 2023 or later.

Bottom line: if you want strong long-term results at a very low price, Bright Start should be your first stop—and, for many Wyoming families, the final decision.

2. Utah my529: the custom builder’s dream

Utah’s plan stands out for one reason: control.

Where most 529s offer three or four preset tracks, my529 lets you design a portfolio from more than twenty Vanguard and Dimensional funds. Want 70 percent U.S. stocks, 20 percent international, and 10 percent TIPS? You can set the exact mix.

That freedom still comes at a low cost. Utah’s program fee is 0.09 percent, and the cheapest all-index blend lands near 0.10 percent total, placing it beside Bright Start. Morningstar has rewarded that mix of autonomy and thrift with a Gold rating every year for more than a decade.

Opening an account is simple, and no deposit is required to start. The interface looks slightly more technical than others, yet clear tutorials guide you through each slider and toggle.

Utah my529 custom portfolio builder interface screenshot.

If you enjoy fine-tuning asset allocations or just value flexibility, my529 will feel like home.

3. New York 529 Direct Plan: pure index investing at 0.11 percent

If you want Vanguard index funds without extra bells, whistles, or hidden fees, New York is a straight path.

Every portfolio in the plan—age based, static, or single asset—costs 0.11 percent all in. No tiered pricing, and no surprises. That consistency means you never wonder if a fancier option carries a higher expense ratio.

The lineup is intentionally lean. Three age-based tracks (aggressive, moderate, conservative) glide from stocks to bonds as college nears. Static choices cover 100 percent equity, bond, or balanced mixes, plus a cash-like option. All rely on Vanguard index funds, so performance mirrors the broad market, and Morningstar awards the plan a Silver medal for cost control and oversight.

Usability matches the investment philosophy: clean and uncluttered. Open an account with as little as one dollar, set up auto-deposits in minutes, and share a UGift link for birthdays. The site skips flashy calculators, which keeps the process friction free.

For Wyoming savers who believe broad-market index investing wins over time, New York delivers that strategy at a price few rivals can match.

4. California ScholarShare 529: tech friendly, ESG ready, and still cheap

ScholarShare feels like it was built by product managers who love index funds. The site is sleek, the mobile app is genuinely useful, and portfolio fees are tiny.

California ScholarShare 529 sleek dashboard and mobile app screenshot.

Choose the passive enrollment tracks and pay as little as 0.05 percent a year—about five dollars on ten thousand. Even the active and ESG portfolios stay below 0.40 percent, so cost control stays in place.

Choice here is broad. You can toggle between Passive, Active, or Socially Responsible versions of each target-date portfolio, or park short-term money in a principal-protected option backed by TIAA. That flexibility lets you match both risk tolerance and personal values without changing platforms.

California adds perks Wyoming families can still enjoy, such as its annual 5/29 Day bonus for new accounts. With no state tax deduction in either state, the only thing that matters is plan quality.

If you want an intuitive interface, the option to lean into ESG, and low fees, ScholarShare is an easy pick.

5. Nevada Vanguard 529: comfort food for index investors

Sometimes you want the brand you already trust. Nevada’s Vanguard plan meets that need while keeping fees low.

Average portfolios cost about 0.14 percent, and the broad U.S. equity option drops to 0.12 percent. Those rates are not the absolute floor, yet the performance gap is too small to matter.

The offer is simple: three risk-based age tracks, six static mixes, and several single-fund options, all built with the same Vanguard funds you may already hold in an IRA. Log in to Vanguard for brokerage or retirement accounts, and your 529 appears on the same dashboard. One login, one statement, and no extra steps.

Usability is classic Vanguard: plain, reliable, and slightly spartan. Open an account with fifty dollars (twenty-five if you automate), link your bank, and you are ready. Upromise cashback deposits are a quick toggle for anyone who enjoys coupon-clipping on autopilot.

For Wyoming families already living in Vanguard world, choosing Nevada means no new learning curve and no fee surprises. It is the financial equivalent of ordering a favorite dish—you know what you will get, and it satisfies every time.

6. Ohio CollegeAdvantage: low-fee workhorse with a rare stable-value fund

Ohio offers one of the most versatile 529 menus in the country. Costs stay modest; most index options sit near 0.14 percent, yet the plan adds features few rivals match.

The headline perk is the Fifth Third 529 Savings Account, an FDIC-insured option that protects principal even when bond funds slip. If your child is in high school and you dislike market swings, that guaranteed bucket can ease stress.

Beyond that, you may toggle among pure Vanguard index tracks, blended portfolios that include active managers such as Dodge & Cox, or single-fund choices that tilt toward small caps or TIPS. Everything appears on one clean dashboard and opens with twenty-five dollars.

Customer experience scores well. Phone representatives work for the Ohio Tuition Trust Authority, not a generic call center, so answers come quickly and clearly. Gifting is simple too; a personalized link channels birthday money straight into the account.

For families who want both insured safety for near-term dollars and low-cost growth for long-term dollars, CollegeAdvantage delivers both in one place.

7. Virginia Invest529: feature rich and future proof

Virginia’s plan is one of the most versatile options on the market. Low-cost index tracks sit beside actively managed blends, ESG portfolios, and a tuition-inflation option for in-state families. Choose the features you need and ignore the rest.

Stay with the Index Enrollment series and total expenses hover near 0.15 percent. Select an active or specialty sleeve and costs remain well below the industry’s old one-percent norm. That price flexibility lets you dial cost and complexity to taste without switching plans.

Performance keeps pace. Morningstar awards Invest529 a Bronze rating for dependable oversight and a track record that lands near the top third of peers over five and ten years. The index track delivers benchmark results minus a small fee, while the active blend adds measured risk for savers seeking extra upside.

User experience scores high. There is no minimum to open, the account wizard takes less than ten minutes, and the mobile app offers a clean snapshot of every beneficiary. A built-in gifting portal collects contributions from relatives, and published guidance on the new 529-to-Roth rollover rule makes leftover funds easy to redeploy.

If you like the idea of starting simple today and adding ESG, active funds, or cash-like options later, Invest529 gives you that runway while keeping fees honest and navigation smooth.

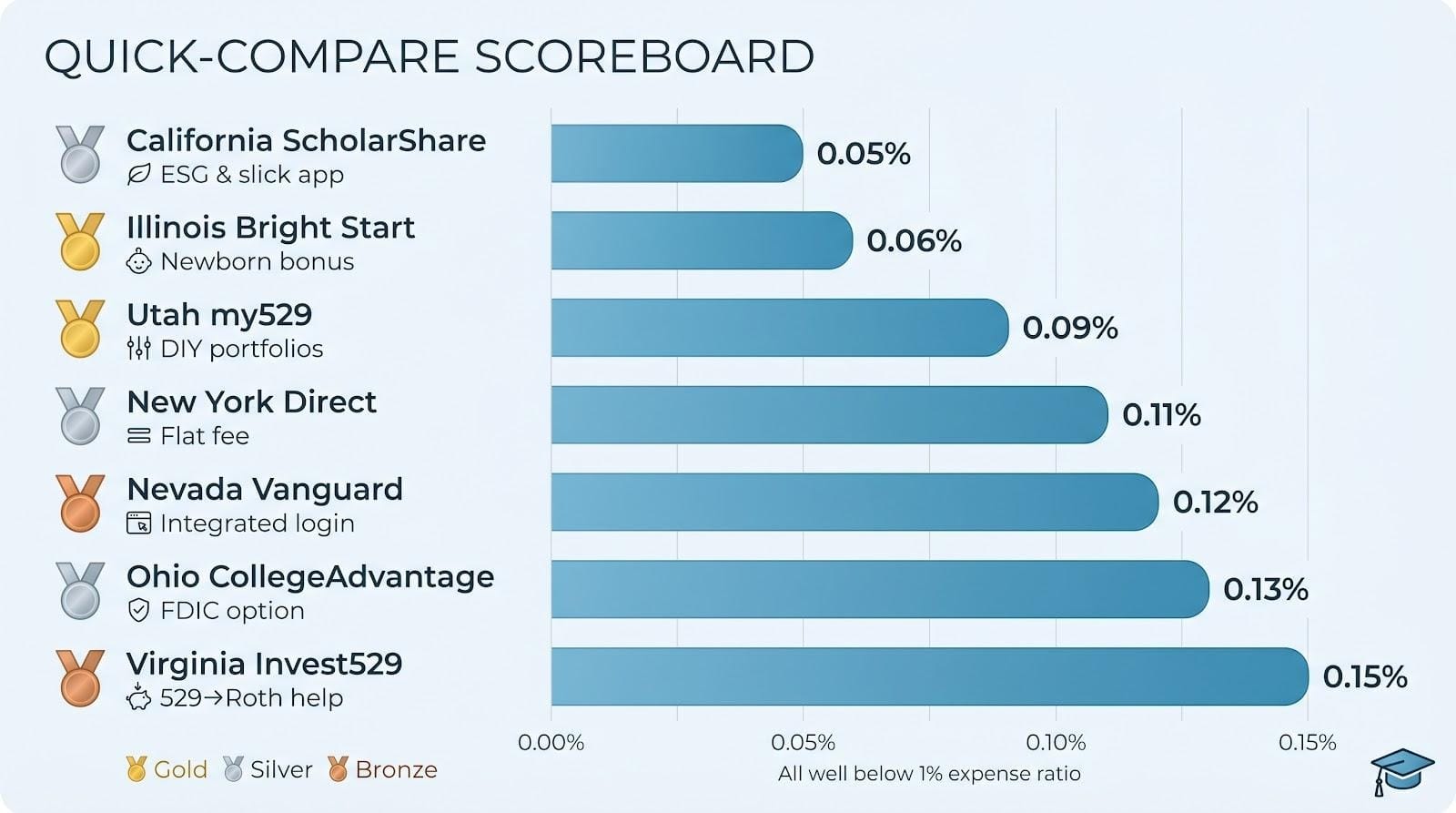

Quick-compare scoreboard

Numbers tell their own story, so the table below lines up the seven plans on a single line of scrimmage.

A quick glance shows why Wyoming savers hold an advantage: each plan charges a fraction of the old one-percent norm while adding a unique twist, from Utah’s DIY flexibility to Ohio’s insured bucket.

Use the table as a gut check. Circle the perk that matters most to you, then decide whether another plan’s slightly lower fee outweighs that feature. In most cases the winner will jump off the page. When it does not, the next section walks you through a decision path to break the tie.

How to pick the right plan for your family

Choosing among seven strong options can feel overwhelming, yet one will fit your situation best.

Start with cost. If squeezing every basis point matters most, focus on Illinois, Utah, or New York. At 0.06 to 0.11 percent, these plans keep more of your earnings compounding for college.

Next, weigh convenience. Already manage money at Vanguard? Nevada places your 529 on the same screen. Prefer a mobile-first experience? California’s interface tops the list.

Then, review features you cannot add later. Need a guaranteed place to park senior-year tuition? Ohio’s FDIC-insured Fifth Third option is rare. Want environmental or social screens? California and Virginia supply ESG choices without extra accounts.

Finally, consider your own habits. If you enjoy fine-tuning asset mixes, Utah’s custom builder offers that flexibility. If you prefer to “set it and forget it,” New York’s age-based tracks handle the shifts for a flat 0.11 percent.

Run through those four filters—cost, convenience, unique features, and personal style—and one plan will usually stand out. If two remain, open each application in a browser tab and choose the signup flow that feels easier. A simple path today often keeps you contributing tomorrow.

Your biggest 529 questions, answered

Is Wyoming ever going to launch its own 529?

There is no bill in the pipeline and little incentive for lawmakers to create one. The state has no income tax to offset, so residents lose nothing by shopping nationally.

Will a 529 hurt my student’s financial-aid chances?

A parent-owned 529 counts as a parental asset on the FAFSA. That reduces aid eligibility by at most 5.64 percent of the account value, compared with a 20 percent hit on a student-owned account. Exploring goal setting finance principles helps parents align their 529 savings strategy with realistic financial aid expectations and long-term college cost planning. In practice, every thousand dollars saved lowers need-based aid by about fifty-six dollars and forty cents.

What if my child earns a full scholarship?

You have three solid options:

- Switch the beneficiary to another family member.

- Roll up to thirty-five thousand dollars into the student’s Roth IRA under SECURE 2.0 rules. Understanding investing and insurance fundamentals helps families make informed decisions about rolling over 529 funds into retirement accounts and managing long-term financial planning effectively.

- Withdraw the scholarship amount penalty-free (you still owe income tax on the earnings portion).

Can I own more than one plan?

Yes. Federal rules set no limit on the number of 529s per beneficiary. Most families manage fine with one, yet you could keep growth dollars in Utah’s custom portfolio and park senior-year tuition in Ohio’s FDIC-insured bucket.

Do I have to use the plan’s age-based fund?

No. Every plan on our list lets you mix static portfolios or single-fund options. Age-based tracks are simply the easiest default for hands-off savers.

How hard is it to move plans later?

A direct rollover (plan A wires money straight to plan B) is tax free once every twelve months per beneficiary. Because Wyoming offers no deduction, you skip the recapture penalties that can trip up taxpayers in other states.

Conclusion

Keep these answers close, but do not let questions delay you. Opening a low-fee plan today beats waiting another year for a “perfect” answer.