DuPont Analysis and ROE Decomposition for Banks and NBFCs

In Financial Ratio Analysis - Liquidity, Profitability & Leverage, you learned to read ratios like ROE, margins, turnover and leverage separately. DuPont Analysis answers the next question: if two companies show similar Return on Equity, why are they getting there in different ways? This matters in interviews because banks and Non-Banking Financial Companies, or NBFCs, can report comparable ROE while relying on very different combinations of margin, asset efficiency and leverage.

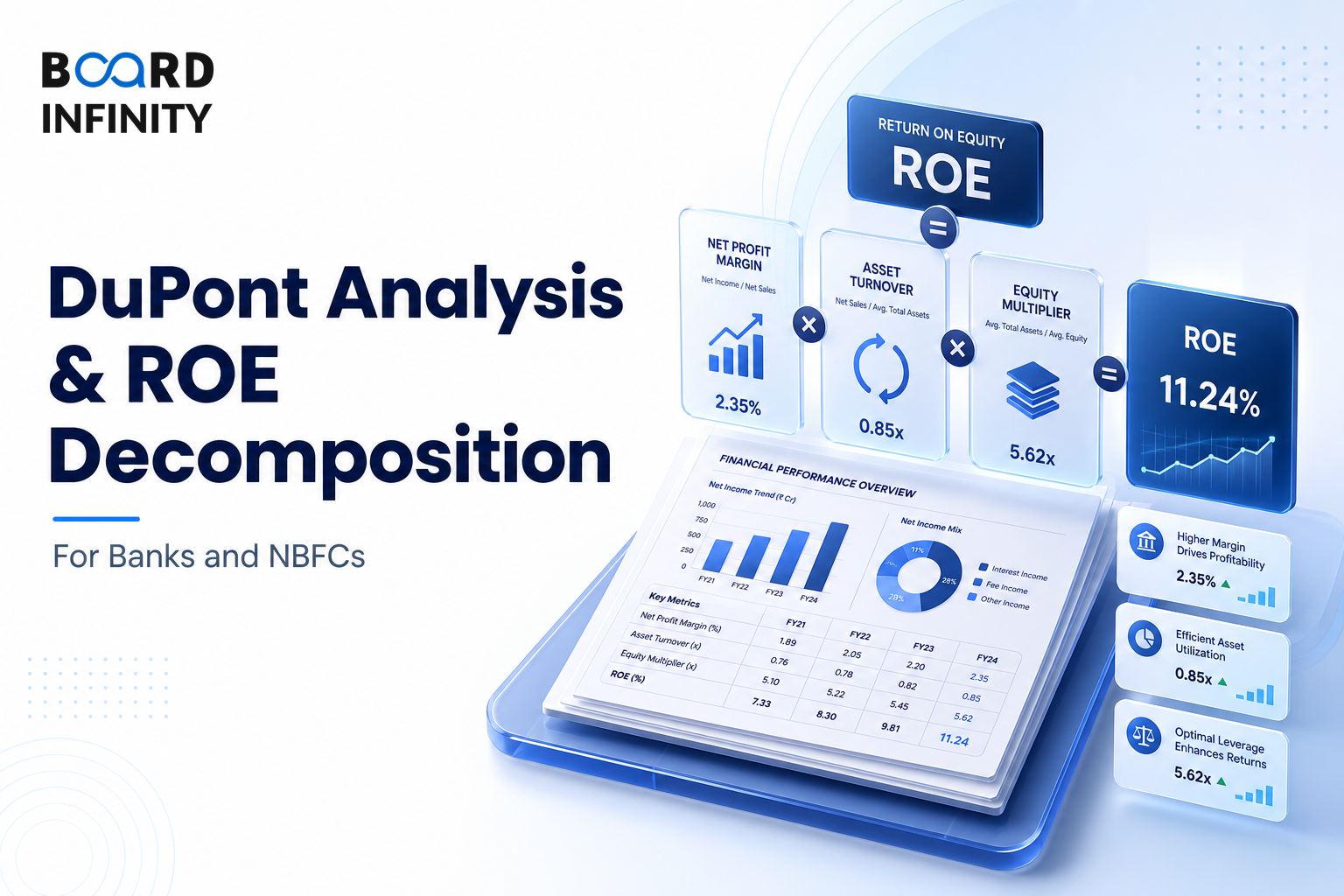

- Return on Equity, or ROE, measures how effectively a company uses shareholders' capital: Net Income divided by Equity.

- DuPont Analysis decomposes ROE so you can identify whether performance is driven by taxes, interest cost, operating margin, asset turnover or leverage.

- The 5-factor formula is: ROE = Tax Burden × Interest Burden × EBIT Margin × Asset Turnover × Equity Multiplier.

- For banks and NBFCs, the equity multiplier is important, but it is not always the main reason for superior ROE.

- In the illustrative data, Bajaj Finance has the highest ROE at 25.3%, driven by higher asset turnover and stronger EBIT margin, not leverage.

- SBI has the highest equity multiplier at 14.1x, but its EBIT margin of 26% compresses ROE.

- In interviews, do not stop at "higher ROE is better"; explain which lever is creating the ROE and whether that lever looks operational, financial or structural.

Big Picture - ROE as a Chain of Five Levers

DuPont Analysis turns one headline profitability number into a diagnostic map. Instead of treating ROE as a single result, it shows how tax impact, interest impact, operating profitability, asset efficiency and leverage combine to produce shareholder returns.

5-Factor DuPont: ROE = Tax Burden × Interest Burden × EBIT Margin × Asset Turnover × Equity Multiplier.

In the illustrative comparison, HDFC Bank has ROE of 16.8% while SBI has ROE of 15.2%. The numbers are close, but the drivers differ: SBI uses much higher leverage with an equity multiplier of 14.1x versus HDFC Bank at 9.2x, while HDFC Bank has a stronger EBIT margin of 38% versus SBI at 26%. The strategic "so what" is that management focus would differ: one case points toward profitability improvement, the other toward understanding leverage and operating efficiency together.

What ROE Tells You - and What It Hides

Return on Equity, or ROE, is calculated as Net Income divided by Equity. It tells you how effectively a company uses shareholders' capital to generate profit.

On its own, ROE is useful but incomplete. A company can improve ROE through better margins, faster use of assets or more leverage. In banks and NBFCs, this distinction is especially important because leverage is a key differentiator, but the source content shows that leverage alone does not explain all ROE differences.

The simpler DuPont view expresses ROE as Net Margin × Asset Turnover × Equity Multiplier. The 5-factor version goes deeper by splitting margin into tax, interest and operating effects. That is why it is more useful for interview discussions on financial institutions where interest cost and leverage matter.

The 5-Factor DuPont Formula, Explained

The 5-factor model breaks ROE into five linked ratios. Multiplying them produces ROE, because the intermediate terms cancel out and leave Net Income divided by Equity.

The power of the formula is not just mathematical. It gives you a management diagnosis. If ROE is weak because of EBIT margin, the discussion is about operating profitability. If it is weak because of asset turnover, the question becomes asset productivity. If it depends heavily on the equity multiplier, the business is leaning more on leverage.

Comparing HDFC Bank, SBI and Bajaj Finance

The following figures are illustrative and approximate for educational purposes only, as stated in the source. They are useful because they show how three named financial institutions can produce different ROE outcomes through different combinations of the five DuPont levers.

The table shows why DuPont is better than looking at ROE alone. Bajaj Finance has the highest ROE at 25.3%, but it does not have the highest equity multiplier. Its ROE is supported by a higher EBIT margin of 42% and higher asset turnover of 0.12x.

SBI, on the other hand, has the highest equity multiplier at 14.1x, but its EBIT margin of 26% and asset turnover of 0.06x hold back ROE. HDFC Bank sits between the two on ROE, with a stronger EBIT margin than SBI and lower leverage than SBI.

How to Read Each Lever in an Interview

When an interviewer gives you ROE data, do not jump directly to a judgment. Use the five factors to separate quality of earnings from balance sheet structure. The same ROE can be created by very different paths.

A strong answer should connect the ratio to a business implication. For example, "SBI has high leverage" is incomplete. A better answer is: "SBI has the highest equity multiplier at 14.1x, but the benefit is offset by a weaker EBIT margin of 26%, so leverage alone does not translate into the highest ROE."

Worked Example - Diagnosing Bajaj Finance Versus HDFC Bank

Assume an interviewer asks why Bajaj Finance has higher ROE than HDFC Bank in the illustrative data. The problem is not to repeat the ROE number, but to identify the levers that explain the gap.

The practical conclusion is clear: Bajaj Finance's superior ROE in the source is explained by stronger asset turnover and EBIT margin. This is the kind of answer that shows financial reasoning rather than formula memorisation.

Why DuPont Matters More for Banks and NBFCs

The source highlights that DuPont is essential for comparing banks and NBFCs where leverage is a key differentiator. Financial institutions often operate with large asset bases relative to equity, so the equity multiplier can meaningfully affect ROE.

However, the same source also shows the nuance: the highest leverage does not automatically create the highest ROE. SBI has the highest equity multiplier at 14.1x, but Bajaj Finance has the highest ROE at 25.3% because its EBIT margin and asset turnover are stronger in the illustrative data.

For banks and NBFCs, always check whether ROE is margin-led, efficiency-led or leverage-led. A leverage-led ROE may look strong at the headline level, but DuPont helps you explain whether operating profitability and asset use are supporting it.

Reusable DuPont Answer Template

Use this structure whenever you are given ROE data in a placement, finance or banking interview. It keeps your answer complete without becoming mechanical.

Structuring a DuPont Analysis & ROE Decomposition Interview Answer

"HDFC Bank, SBI and Bajaj Finance show different ROE levels. How would you use DuPont Analysis to explain what is driving the difference?"

The best candidates do not just recite the formula. They use the formula to say what kind of ROE it is: margin-led, efficiency-led or leverage-led.

Conclusion

DuPont Analysis makes ROE useful by showing why it happens. For banks and NBFCs, the key takeaway is to decompose before judging: superior ROE may come from leverage, but in the given comparison Bajaj Finance's advantage comes from asset turnover and EBIT margin.

The most frequent error is saying that higher leverage automatically means higher or better ROE. SBI has the highest equity multiplier at 14.1x, but its ROE is 15.2% because weaker EBIT margin compresses the result. In interviews, this costs points because it ignores the diagnostic purpose of DuPont Analysis.